2020 was a rollercoaster year for the European smartphone market. The COVID-19 pandemic hit the region hard, resulting in both supply and demand side issues. Meanwhile, economic concerns and employment worries led to consumers saving rather than spending, and widespread lockdowns meant that many consumers were unable or unwilling to visit retail stores and buy new devices.

2020 was a rollercoaster year for the European smartphone market. The COVID-19 pandemic hit the region hard, resulting in both supply and demand side issues. Meanwhile, economic concerns and employment worries led to consumers saving rather than spending, and widespread lockdowns meant that many consumers were unable or unwilling to visit retail stores and buy new devices.

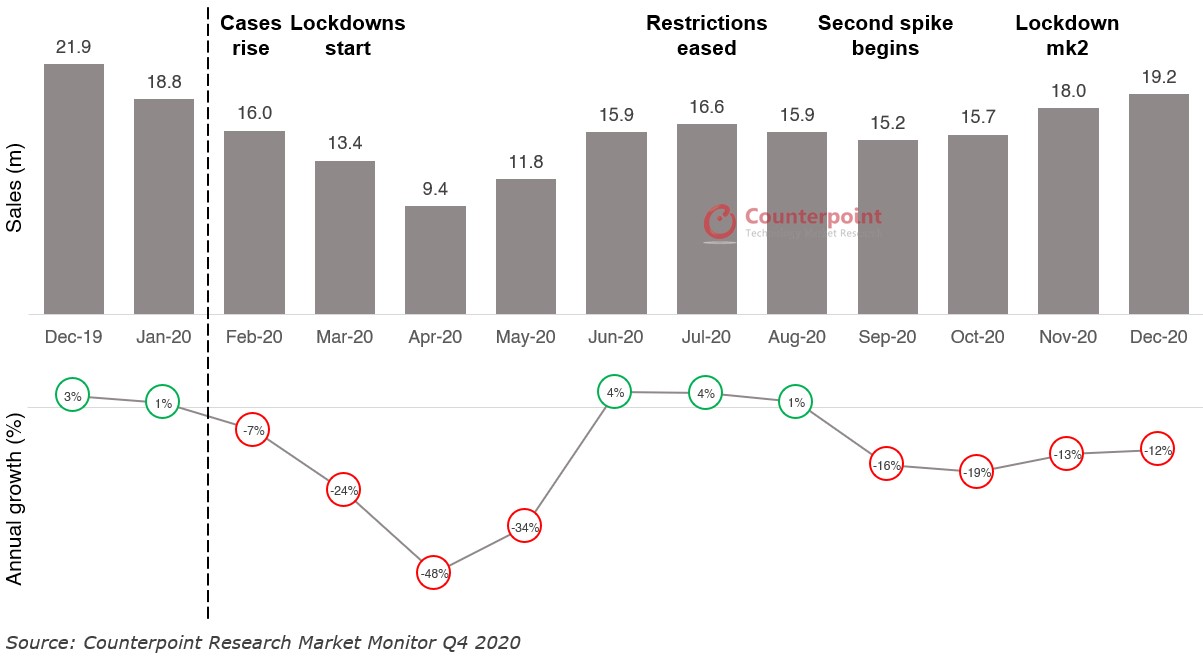

Speaking about the overall market, Counterpoint Research’s Associate Director, Jan Stryjak said, “April was the worst month of the year, with sales down almost 50% on 2019. Declining cases and easing restrictions led to a recovery over the summer, but the virus came back with a vengeance. COVID-19 cases rose in September leading to new lockdowns across Europe from November. The end of the year, therefore, saw the market decline again, despite the best efforts of Apple (see below). Overall, 2020 saw the European smartphone market shrink by 14% versus 2019.”

Exhibit 1: Covid-19 Impact on European Smartphone Sales

Stryjak added, ‘In addition to the pandemic, US sanctions on Huawei harmed its ability to bring new products to market and produce existing products in volume. This has created opportunities for some smartphone makers, so while the 2020 was difficult, there were winners as well as losers.’

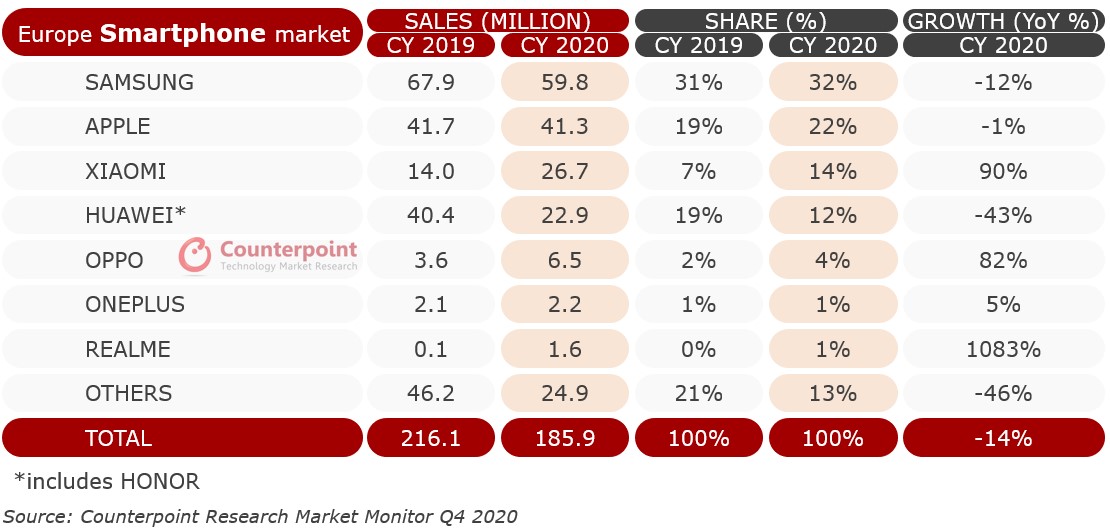

Exhibit 2: Full year European Smartphone Sales Market Share and Growth

A year to remember:

- Xiaomi was the major success story in Europe in 2020, becoming the third largest OEM in the region at expense of Huawei. Strong performance in both Spain and Italy resulted in significant share gains over the year (reaching 28% and 17% of smartphone sales in Q4 2020 respectively), driving overall annual growth of 90% for the year. Xiaomi’s challenge is now to replicate this growth in other areas, particularly more premium markets like France, Germany and the UK: the launch of its flagship Mi 11 in February 2021 should help.

- Apple may have declined slightly in 2020, but this doesn’t tell the full story. The decision to delay the launch of the iPhone 12 appears to have paid off, for two reasons. First, it gave the iPhone 11 and iPhone SE the opportunity to demonstrate remarkable longevity, selling continuously well in many markets throughout the year. And second, it built up demand for the new device which, when finally launched in October, sold spectacularly. In fact, the iPhone 12 was Apple’s most successful device launch to date, and drove Apple to a record share high of 30% in Q4 2020.

- Oppo entered the European market in 2018, but 2020 was the year it gained some serious momentum. Partnerships with Europe’s largest operator groups – namely Vodafone, Telefonica, Orange and Deutsche Telekom – mean that Oppo’s devices are stocked in the vital operator channel throughout Europe. While sales are still relatively modest in the region, market share has doubled over the year, and a strong fourth quarter puts Oppo in good stead for 2021.

- Realme was the fastest growing brand in Europe in 2020, with sales increasing more than ten-fold on 2019. Its strong value proposition has led to good growth in more price-conscious markets such as Italy, Spain and across Eastern Europe.

A year to forget:

- Huawei’s inability to produce competitive smartphones thanks to US sanctions means the vendor has all but exited the European smartphone market. Yes, it briefly overtook Apple to become the region’s second largest vendor (behind Samsung) in May, but that was more to do with the premium end of the market taking the brunt of the COVID-19 impact, and Apple being mid-way between launches at that point. Over the year, Huawei’s share has fallen from 15% in January to 5% in December, and there is no reason to expect the trajectory to change in 2021.

- Samsung had a tough year. Even though it managed to grow share slightly, this was because its sales didn’t decline as much as the total market. Samsung didn’t capture as much of Huawei’s declining market share as perhaps it would have expected, having faced significant challenges from all directions. First, sales of its flagship Galaxy S20 never really took off – it was regularly outsold in Europe by Samsung’s own mid-range Galaxy A51 and A71 models, as well as devices from Apple and Android competitor Xiaomi (like the Redmi 8/Note 8 and Redmi 9/Note 9 series). Second, competition in Europe has never been greater, with numerous relatively new vendors (see above) fighting it out to capture market share once held by Huawei. And third, Apple’s latest offering – the iPhone 12 – is (finally) 5G enabled, which means Samsung’s near monopoly of the premium 5G segment is over. Samsung’s new flagship Galaxy S21 should do better than the S20 and will likely be the leading Android premium smartphone in Europe in 2021, but Samsung has its work cut out.

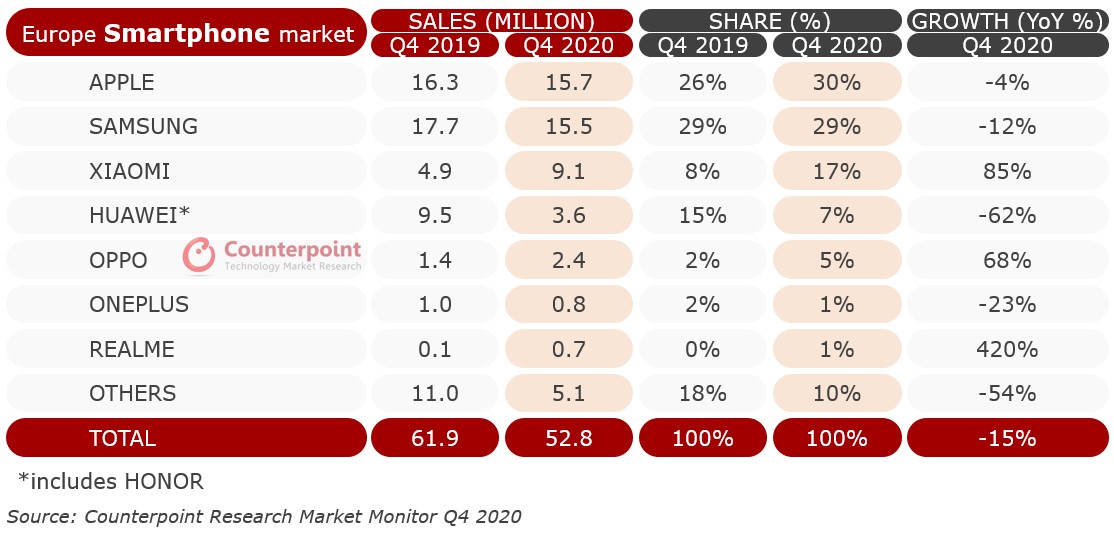

Exhibit 3: Q4 European Smartphone Sales Market Share and Growth

A relatively successful Christmas period in Europe hinted at a positive outlook for 2021. Research Analyst, Ankit Malhotra said, “The market ended the year on a strong note in Q4 backed by the demand for the 5G iPhone. This strong momentum is expected to continue in Q1 2021 as sales of iPhone 12 spill over to the next quarter and the Samsung Galaxy S21 is launched. The rush of flagships in Q1 from Samsung and Apple, the eventual easing of lockdowns and expectations of an economic recovery will then lay the foundation for a swift recovery of the market in 2021. Along with that, we will need to keep a keen eye on the development of 5G and the performance of new arrivals like Xiaomi, Oppo, OnePlus, Vivo and realme as they attempt to fill the gap left by Huawei.”