Qualcomm ended the fiscal year with a huge bang, growing yearly revenues by 43% despite the global shortage of semiconductor components and continued global COVID-19 infection waves.

The key to Qualcomm’s revenue growth was its ability to dual and triple source manufacturing of key components, namely its Snapdragon 800 series SoC’s and its premium 5G modem.

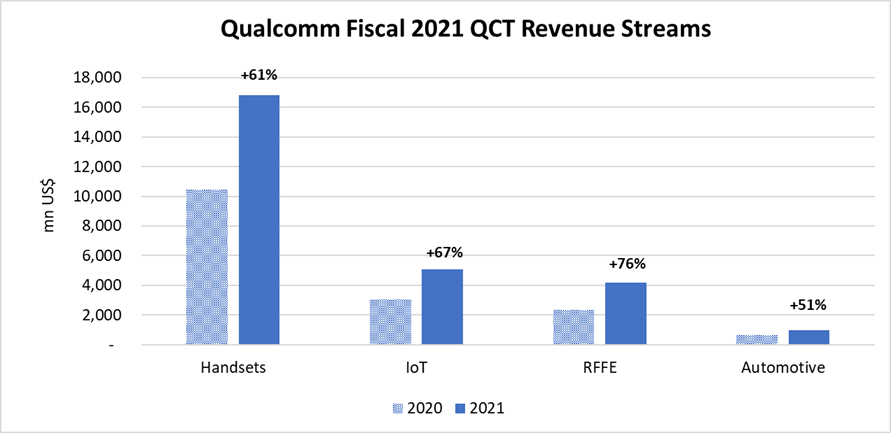

Besides 21% growth within Snapdragon premium tier products, Qualcomm’s RF front-end components, automotive, and IoT components have grown impressively to become, cumulatively, a $10bn business. This has reduced the company’s dependence on Apple and mitigates some of the risk around if Apple eventually moves to making its modems in-house.

Other business units also contributed to Qualcomm’s bottom line; areas to watch include its drone platform, WiFi6 and WiFi6E solutions, XR platform, fixed wireless access solutions, wearable SoCs and its TWS solutions.

Source: Company data.

Keys to the quarter and outlook for 2022:

- Global semi constraints continue, and Qualcomm has prioritized high-end / higher margin solutions.

- Dual and triple sourcing has helped but look for semi component shortages to continue through 2022 – especially during the first half of the year.

- New Android premium flagships in 2022 will likely bring in higher ASPs. Android foldables growth is also a growth opportunity in 2022.

- Qualcomm’s licensing division brought in revenues of $6.3 billion. The company is bullish on its innovation within cellular technology and the value of its patent portfolio. It continues to see premium Android OEMs purchase both its 5G SoC’s along with its RF front-end solutions.

- The RF front-end business continues to innovate with new ultraBAW filter technologies. At its most basic, these technology advances improve tuning within higher frequencies. As RF front-end continues to grow more complex, Qualcomm has gained revenue market share within the space.

- WiFi6 / 6E solutions will grow as the consumer electronics industry rolls out the technology advancements into different verticals.

- When XR hits critical mass, Qualcomm will be able to capitalize on greater XR adoption. Qualcomm is currently powering over 50 XR devices and most of the best-selling devices. Qualcomm also has interesting design wins within smaller verticals such as Peloton bikes and the Amazon ASTRO robot.

- Qualcomm’s fixed wireless access solutions will gain momentum as Verizon, T-Mobile, AT&T and other global operators’ role out the broadband option to consumers.

- Qualcomm’s automotive business unit grew 44% and Qualcomm remains aggressive in the space, growing outside of infotainment solutions. The company’s $4.5bn acquisition of the Swedish automotive technology company Veoneer will help to accelerate bringing new solutions to the market.

- Qualcomm IoT services suite supports over 30 verticals. Retail and digital signage continues to stay under the radar but the company is delivering to leading firms in the space such as Square, Clover, Honeywell and Panasonic. Qualcomm has also won IoT service contracts from cities such as New Orleans. IoT as a service to municipalities is a key area to watch.

- mmWave continues to roll out in the US and Japan. Qualcomm is the key supplier. It will be key to watch when China rolls out the technology. MediaTek may have solutions by the time China begins rolling out mmWave in earnest.

Finally, headwinds to watch (with varying effects on the company):

- Google (and other OEMs) using their own silicon for smartphones. Google global market share likely to remain under 1% and its ambition of growing the Android user base will not affect Qualcomm. Qualcomm remains the key supplier to Android premium and mmWave market. It also powers other Google products.

- Samsung Exynos could challenge Qualcomm within the $200-$400 price segments. There will be a competitive fight within this price segment.

- MediaTek remains a strong competitor and has grown to become the largest smartphone SoC supplier in the market. Qualcomm has growing premium, 8-series momentum and should continue to lead within premium and the growing foldables market. Battle will remain fierce within Dimensity 700/800 series and Qualcomm 600 and 400 series. Ability to supply in 1H2022 will be key. India, APAC, LATAM, and MEA will be key battlegrounds to watch.

- The China market continues to be sluggish. However, 5G sell through according to Counterpoint Premium Market Pulse, remains over 70%. OPPO, vivo, and Xiaomi have moved to supplying more 5G and higher-end devices. There will be a battle with MediaTek for design wins—especially within China.

- Apple, Samsung, and Xiaomi remain top customers of Qualcomm. Considerable market share declines of any of the three would be a headwind.